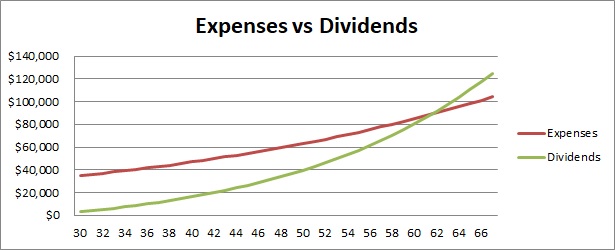

The different struggles for different income groups

$2K-$3K income

Having conversions with my others makes matter worse. I've seen people struggling with finances. For those who have low income of $2K+ to $3K+, they are mostly living from paycheck to paycheck. If you're single and young its ok but those at my age or older are mostly married or have kids. Many of them are waiting for their pay to come in each month and some even have to rely on government subsidies to survive. Some have to take loan just to survive the month.

$3K-$5K income

This is an income group where many middle class workers are in. $3K is probably too low but the median is around $4K-$5K to be sufficient. Singapore's median gross monthly income from work is $5,070 in 2022. This includes employer CPF contributions so the actual monthly income should be lower at about $4106. The take home pay is then $3285. For average (mean) gross monthly income, it is higher at $5832 (including employer CPF). Excluding employer CPF will be around $4732 and take home pay is $3779. If its only a single income supporting a household with 1 kid, this is barely enough. From my conversations with my peers, I've seen people who are earning $4K plus and still struggling with their finances. While most months they will have enough to live by, some month they will have to tighten their belts when they need a sum of money to replace faulty home appliances etc. Another thing to note is that the median and mean gross monthly income already includes commissions and bonuses so the actual basic gross income will be lower.

$5K-$8K income

This is probably quite a big range and can make a difference between someone earning $5K vs someone earning $8K which is much more comfortable. However, I do notice a trend where people who earn more will generally spend more also either they buy a car, go for more overseas trip, upgrade to private property, eat out at restaurants more and generally have higher standards of lifestyle. This group of people will still think that money is not enough to maintain their standard of living and worry about retirement if they need to upkeep this lifestyle.

$8K and above income

Those who earn above $8000 are in the top 20% of earners in Singapore based on the statistics from MOM. I know of a few peers in this category and they are fairly comfortable in life. However, because of current economic uncertainty, the fear of retrenchment for this group of people can be scary as they would probably be in higher management position and if they were to get retrenched, they will be worried if they cannot find a job easily as there are lesser higher management jobs available as compared to a middle management position.

Do You Struggle in your finances?

At every stage of life, we have something to worry about. I get depressed once in awhile when I compare myself to others and in Singapore, it seems like we can never earn enough. When we thought that we are comfortable, someone else seems to have a better life and somehow, the stress of keeping up strikes again. Someone would have a better house, better car, living a seemingly better life. While competition can be healthy sometimes to push ourselves to be better, its what makes us unhappy in life.

Do I still believe in financial freedom? I think its getting harder with the desired Singapore lifestyle and inflation going up. The struggles are real as a Singaporean.